Maximize Savings: Comparing 2026 Medicare Part D Plans for Prescription Costs

Anúncios

Maximize Savings: Comparing 2026 Medicare Part D Plans for Prescription Costs

Navigating the complex world of Medicare can be challenging, especially when it comes to prescription drug coverage. With the 2026 Medicare Part D plans on the horizon, understanding your options and making informed choices is more critical than ever. For many, prescription drug costs represent a significant portion of their healthcare expenses. By diligently comparing 2026 Medicare Part D plans, you have the potential to save up to 15% or even more on your annual medication expenditures. This comprehensive guide will walk you through everything you need to know to effectively compare plans, identify the best fit for your needs, and ultimately keep more money in your pocket.

Anúncios

Understanding Medicare Part D: A Foundation for Savings

Before diving into the specifics of comparing 2026 Medicare Part D plans, it’s essential to have a solid understanding of what Part D entails. Medicare Part D is the prescription drug benefit offered through private insurance companies approved by Medicare. These plans help cover the cost of prescription drugs, both brand-name and generic. While all Part D plans must follow certain rules set by Medicare, the specific drugs covered, the costs, and the pharmacies in their network can vary significantly from one plan to another. This variability is precisely why comparison is key to maximizing your savings.

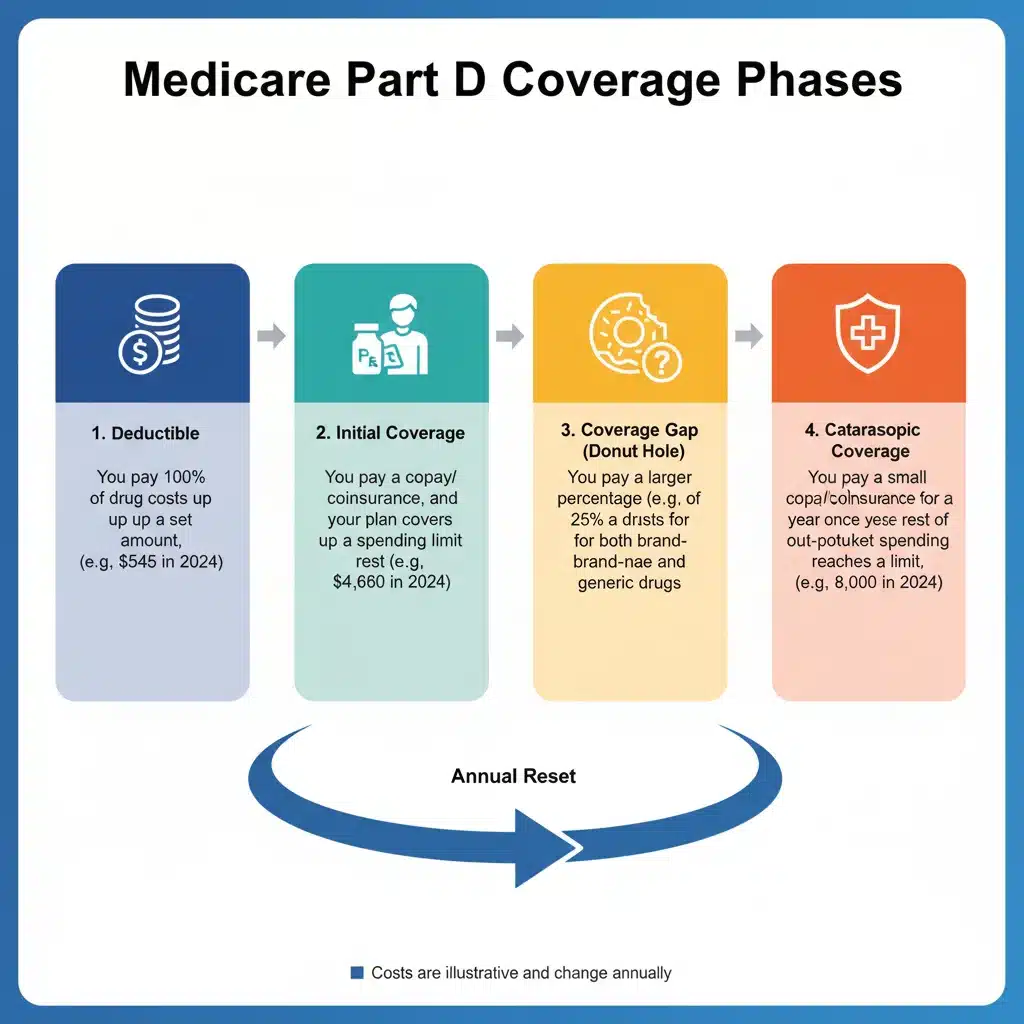

The Four Phases of Part D Coverage

Most Part D plans have four distinct phases of coverage, and understanding them is crucial for predicting your out-of-pocket costs throughout the year:

Anúncios

- Deductible Phase: During this phase, you pay the full cost of your prescriptions until you meet your plan’s deductible. Not all plans have a deductible, and the amount can vary. For 2026, expect adjustments to the standard deductible limits.

- Initial Coverage Phase: After meeting your deductible (if applicable), you pay a copayment or coinsurance for your prescriptions, and your plan pays the rest. There’s a limit to how much the plan will pay in this phase.

- Coverage Gap (Donut Hole): Once your total drug costs (what you and your plan have paid) reach a certain limit, you enter the coverage gap. Historically known as the ‘donut hole,’ this phase required you to pay a higher percentage of your drug costs. Thanks to the Affordable Care Act (ACA) and subsequent legislation, the out-of-pocket costs in the coverage gap have been significantly reduced. For brand-name drugs, you’ll pay 25% of the cost, and the manufacturer pays 70%, with the plan paying 5%. For generic drugs, you’ll pay 25% of the cost, and the plan pays 75%.

- Catastrophic Coverage Phase: After your out-of-pocket spending reaches a certain threshold (which includes your deductible, copayments, and what you pay in the coverage gap), you enter the catastrophic coverage phase. In this phase, you typically pay a very small copayment or coinsurance for your drugs for the remainder of the year.

Understanding these phases is the first step in effectively comparing 2026 Medicare Part D plans, as the cost structure of each phase can differ between plans, directly impacting your potential savings.

Why Comparing 2026 Medicare Part D Plans is Essential

The landscape of prescription drug coverage is dynamic. What might have been the best plan for you in 2025 may not be the optimal choice for 2026. Insurance companies adjust their formularies (list of covered drugs), premiums, deductibles, copayments, and preferred pharmacies annually. Failing to re-evaluate your plan can lead to unexpected and potentially higher out-of-pocket expenses. Here’s why a thorough comparison of 2026 Medicare Part D plans is crucial:

- Changes in Formularies: Your current medications might be removed from your plan’s formulary, moved to a higher cost-sharing tier, or require prior authorization in the new year.

- Premium Adjustments: Plan premiums can increase or decrease. While a lower premium might seem attractive, it’s vital to consider the overall costs, including deductibles and copayments.

- Deductible and Copayment Changes: These out-of-pocket costs can shift, impacting your initial and ongoing expenses.

- Pharmacy Network Updates: Your preferred pharmacy might no longer be part of your plan’s preferred network, meaning higher costs for your prescriptions.

- Changes in Your Health Needs: If your health condition has changed, or you anticipate new medications, your current plan might no longer provide the most cost-effective coverage.

- New Plan Options: New plans may emerge in your area that offer better coverage or lower costs for your specific drugs.

By actively comparing 2026 Medicare Part D plans, you proactively manage your healthcare budget and ensure you’re not overpaying for your essential medications.

Key Factors to Consider When Comparing Plans

To effectively compare 2026 Medicare Part D plans and achieve significant savings, focus on these critical factors:

1. Your Current Medications (Formulary Check)

This is arguably the most important factor. Create a comprehensive list of all your prescription medications, including dosages and frequency. Then, for each prospective plan, check its formulary to ensure:

- All your drugs are covered: If a drug isn’t on the formulary, you’ll pay 100% of its cost out-of-pocket.

- Your drugs are on a favorable tier: Formularies typically organize drugs into tiers, with Tier 1 (preferred generics) having the lowest copayments and higher tiers (non-preferred brands, specialty drugs) having much higher costs.

- No special restrictions: Some drugs may require prior authorization (your doctor needs to get approval from the plan), step therapy (you must try a less expensive drug first), or quantity limits. These restrictions can impact access and cost.

Use the Medicare Plan Finder tool on Medicare.gov to input your medications and compare how each plan covers them.

2. Total Annual Costs (Premiums, Deductibles, Copayments)

Don’t just look at the monthly premium. A low premium might come with a high deductible or high copayments, leading to higher overall annual costs. Conversely, a higher premium might offer lower out-of-pocket costs for your specific drugs. Calculate the estimated total annual cost for each plan, considering:

- Monthly Premium: The fixed amount you pay each month.

- Annual Deductible: How much you must pay before the plan starts to pay.

- Copayments/Coinsurance: Your share of the cost for each prescription fill in the initial coverage phase.

- Coverage Gap Costs: Estimate your costs if you enter the ‘donut hole.’

The Medicare Plan Finder tool can often provide an estimate of your total annual out-of-pocket costs based on your entered medications.

3. Pharmacy Network and Preferred Pharmacies

Check if your preferred pharmacy (or pharmacies) is in the plan’s network. Many plans have preferred pharmacy networks that offer lower copayments. If you use an out-of-network pharmacy, your costs will be higher, or your drugs might not be covered at all. Consider convenience, location, and the availability of mail-order options if that’s something you use.

4. Star Ratings

Medicare uses a 5-star rating system to evaluate the quality and performance of Part D plans. A 5-star plan indicates excellent quality, while a 1-star plan indicates poor quality. While cost is important, a higher-rated plan often signifies better customer service, fewer complaints, and efficient claims processing. Look for plans with at least 3.5 or 4 stars.

5. Extra Benefits (If Any)

Some Part D plans might offer additional benefits, such as discounts on over-the-counter medications, health and wellness programs, or even a small deductible for certain generic drugs. While these shouldn’t be the primary deciding factor, they can add value if all other factors are equal.

Strategies to Save Up to 15% (or More!) on Prescription Costs

Beyond simply comparing plans, several strategies can help you maximize your savings on 2026 Medicare Part D prescription costs:

1. Annual Review During Open Enrollment

The Annual Enrollment Period (AEP) for Medicare runs from October 15th to December 7th each year. This is your prime opportunity to review and switch your Part D plan for the upcoming year. Even if you were happy with your plan this year, always re-evaluate. Plans change, and so do your needs. A quick review could uncover significant savings for 2026 Medicare Part D.

2. Utilize the Medicare Plan Finder Tool

Medicare.gov’s Plan Finder is an invaluable, free resource. It allows you to enter your medications, preferred pharmacies, and other relevant information to get a personalized comparison of all available Part D plans in your area. It estimates your total annual costs for each plan, making the comparison process much easier and more accurate.

3. Consider a Medicare Advantage Plan (Part C) with Prescription Drug Coverage (MAPD)

Medicare Advantage plans often bundle Part A (hospital insurance), Part B (medical insurance), and Part D into one comprehensive plan. Sometimes, these bundled plans can offer lower overall costs or additional benefits compared to having Original Medicare plus a standalone Part D plan. If you’re open to an Advantage Plan, explore these options when comparing 2026 Medicare Part D coverage.

4. Talk to Your Doctor About Generics or Lower-Cost Alternatives

If your current medications are on a high-cost tier or are not covered, discuss alternatives with your doctor. There might be a generic version or a therapeutically equivalent brand-name drug on a lower tier that could save you money without compromising your health.

5. Explore Patient Assistance Programs (PAPs)

If you have high drug costs, especially for expensive brand-name or specialty drugs, look into Patient Assistance Programs offered by pharmaceutical companies or non-profit organizations. These programs can provide free or low-cost medications to eligible individuals. Your doctor’s office or a local SHIP (State Health Insurance Assistance Program) counselor can help you find these resources.

6. Use Mail-Order Pharmacies (If Applicable)

Many Part D plans offer lower prices or extended supply options (e.g., a 90-day supply for the cost of two 30-day supplies) through their preferred mail-order pharmacies. If you take maintenance medications, this can lead to substantial savings.

7. Check for Extra Help (Low-Income Subsidy)

If you have limited income and resources, you might qualify for Medicare’s ‘Extra Help’ program, also known as the Low-Income Subsidy (LIS). This program helps pay for Part D premiums, deductibles, and copayments. It can significantly reduce your out-of-pocket costs. You can apply for Extra Help through the Social Security Administration.

8. Review Your Plan’s Explanation of Benefits (EOB)

Regularly review the Explanation of Benefits (EOB) statements from your Part D plan. These documents detail what you paid, what the plan paid, and how much credit you received toward your deductible and out-of-pocket maximum. This helps you track your spending and ensures accurate billing.

Understanding the Impact of Inflation Reduction Act (IRA) on 2026 Medicare Part D

The Inflation Reduction Act (IRA) of 2022 has introduced significant changes to Medicare Part D that will continue to roll out and impact beneficiaries in 2026. These changes are designed to lower prescription drug costs and provide greater financial predictability. When comparing 2026 Medicare Part D plans, keep these IRA provisions in mind:

- $2,000 Annual Cap on Out-of-Pocket Drug Costs: This is a monumental change. Starting in 2025, there will be a $2,000 cap on out-of-pocket prescription drug costs for Part D enrollees. This cap means that once you spend $2,000 out of pocket in a year, you will pay nothing for your covered Part D drugs for the remainder of that year. This eliminates the 5% coinsurance previously required in the catastrophic coverage phase and provides immense financial relief for those with high prescription costs. For 2026, this cap will continue to provide significant protection.

- Lower Insulin Costs: The IRA capped the cost of insulin at $35 per month for Medicare beneficiaries. This provision is already in effect and will continue through 2026, ensuring predictable and affordable insulin costs.

- Vaccines Covered at No Cost: Most adult vaccines recommended by the Advisory Committee on Immunization Practices (ACIP) are covered at no cost under Part D. This includes vaccines for shingles, tetanus, diphtheria, and pertussis (Tdap), and RSV. This benefit began in 2023 and will remain in place for 2026.

- Drug Price Negotiation: While the full impact of Medicare’s ability to negotiate drug prices will take time to materialize, it’s a long-term benefit that aims to lower overall drug costs. In 2026, we may start to see some of the negotiated prices influencing plan costs and formularies.

- Premium Stabilization: The IRA also includes provisions aimed at slowing the growth of Part D premiums. While premiums can still change, the goal is to make them more stable and predictable for beneficiaries.

These changes are critical to consider as they fundamentally alter the financial landscape of 2026 Medicare Part D. The $2,000 out-of-pocket cap, in particular, offers unprecedented protection against high drug costs, making it easier to budget for your medications.

When and How to Enroll or Switch Plans

The primary time to enroll in a 2026 Medicare Part D plan or switch from your current plan is during the Annual Enrollment Period (AEP), which runs from October 15th to December 7th each year. Any changes you make during this period will become effective on January 1st of the following year.

Steps to Enroll or Switch:

- Gather Your Information: Have your Medicare card, a list of all your current medications (including dosage and frequency), and your preferred pharmacies ready.

- Use the Medicare Plan Finder: Go to Medicare.gov/plan-compare. Enter your zip code, your Medicare information, and your prescription drugs. The tool will then show you available plans in your area, estimate your annual costs, and highlight key differences.

- Compare Carefully: Review the results, paying close attention to premiums, deductibles, copayments for your specific drugs, and pharmacy networks. Consider the plan’s star rating.

- Enroll Directly: Once you’ve chosen a plan, you can enroll directly through the Medicare Plan Finder website, by calling the plan directly, or by calling Medicare at 1-800-MEDICARE (1-800-633-4227).

If you’re already enrolled in a Part D plan and switch to a new one during AEP, your old plan will automatically be canceled when your new plan becomes effective on January 1st. You don’t need to contact your old plan to disenroll.

Common Mistakes to Avoid

To truly save up to 15% or more and ensure you have the best coverage for 2026 Medicare Part D, avoid these common pitfalls:

- Not Comparing Annually: Assuming your current plan is still the best option is a costly mistake. Always re-evaluate during AEP.

- Focusing Only on Premium: A low premium can hide high deductibles or copayments. Look at the total estimated annual cost.

- Ignoring the Formulary: The most crucial aspect. If your drugs aren’t covered or are in high tiers, the plan isn’t right for you.

- Not Checking Pharmacy Networks: Make sure your preferred pharmacy is in-network, especially if it’s a preferred pharmacy for lower costs.

- Waiting Until the Last Minute: Start your research early in the AEP (October/November) to give yourself ample time to compare and make a thoughtful decision.

- Not Seeking Help: If you find the process overwhelming, don’t hesitate to contact your State Health Insurance Assistance Program (SHIP), a licensed insurance agent, or Medicare directly for assistance.

Conclusion: Take Control of Your 2026 Medicare Part D Costs

The prospect of saving up to 15% on your prescription costs for 2026 Medicare Part D is a tangible goal with the right approach. By understanding the fundamentals of Part D, diligently comparing plans based on your specific medication needs, considering total annual costs, and leveraging the powerful tools and resources available, you can make an informed decision that protects your health and your wallet. The changes introduced by the Inflation Reduction Act further enhance the financial predictability and security of Part D, especially with the $2,000 out-of-pocket cap starting in 2025.

Don’t let inertia or confusion lead to unnecessary expenses. Mark your calendar for the Annual Enrollment Period, gather your information, and commit to a thorough comparison. Taking these proactive steps will empower you to choose the best 2026 Medicare Part D plan for your unique circumstances, ensuring you receive the medications you need at the most affordable price.

Remember, your health and financial well-being are worth the effort. Start planning now to secure your savings for 2026!