2026 Healthcare.gov Enrollment: Maximizing New Subsidies & Affordability

Anúncios

Navigating the complex world of health insurance can often feel overwhelming, but with the right information, securing affordable coverage for you and your family can be a straightforward process. As we approach the 2026 Healthcare.gov Enrollment period, it’s more crucial than ever to understand the significant changes and new opportunities available, particularly concerning subsidies designed to make health insurance more accessible and affordable than ever before. This comprehensive guide will walk you through everything you need to know about 2026 Healthcare.gov Enrollment, focusing on maximizing new subsidies, understanding eligibility, and ensuring a smooth application process.

The Affordable Care Act (ACA), often referred to as Obamacare, has been instrumental in expanding health insurance coverage across the United States. Healthcare.gov serves as the federal marketplace where individuals and families can compare and enroll in health insurance plans. Over the years, the ACA has undergone various adjustments, and the 2026 enrollment period brings with it enhanced subsidies and expanded eligibility criteria that could significantly reduce your out-of-pocket costs for health insurance premiums.

Anúncios

For many, the cost of health insurance has been a major barrier to obtaining coverage. However, the introduction of new and expanded subsidies aims to alleviate this burden, making quality health insurance plans more attainable for a broader range of incomes. Understanding these subsidies and how they apply to your specific situation is key to making an informed decision during the 2026 Healthcare.gov Enrollment period.

This article will delve into the specifics of these new subsidies, explain who is eligible, provide a step-by-step guide to the enrollment process, and offer valuable tips to help you choose the best plan for your needs. Whether you’re new to Healthcare.gov or a returning enrollee, this guide is designed to equip you with the knowledge and confidence to navigate your health insurance options effectively.

Anúncios

Understanding the Landscape of 2026 Healthcare.gov Enrollment

The 2026 Healthcare.gov Enrollment period is set to build upon the foundation laid by previous years, with a renewed emphasis on affordability and access. The federal government continues to refine the ACA to address the evolving healthcare needs of the population. These refinements often translate into changes in subsidy structures, eligibility requirements, and available plans. Staying informed about these updates is paramount for anyone seeking coverage through the marketplace.

The Evolution of Subsidies: What’s New for 2026?

One of the most impactful aspects of the ACA has been the provision of financial assistance to help lower the cost of monthly premiums and out-of-pocket expenses. These subsidies come in two main forms: Premium Tax Credits (PTC) and Cost-Sharing Reductions (CSRs).

- Premium Tax Credits (PTC): These credits reduce your monthly premium payments. The amount of your tax credit is based on your income, household size, and the cost of a benchmark plan in your area. For 2026, it is anticipated that the enhanced subsidies, which temporarily removed the income cap for eligibility and increased the amount of assistance for many, will continue or be further refined to ensure that no one pays more than a certain percentage of their household income for a benchmark silver plan. This means more individuals and families, including those with higher incomes who previously didn’t qualify, may now be eligible for significant financial help.

- Cost-Sharing Reductions (CSRs): These subsidies help reduce your out-of-pocket costs, such as deductibles, co-payments, and co-insurance. CSRs are only available if you enroll in a Silver-level plan and meet specific income requirements. They effectively make Silver plans more generous, offering better coverage than their standard counterparts at the same premium.

The continuity and potential enhancements of these subsidies for the 2026 Healthcare.gov Enrollment period are critical. They represent a sustained effort to combat rising healthcare costs and ensure that every American has access to essential health benefits. It’s important to remember that these subsidies are typically paid directly to your insurance company, lowering your monthly bill, but you can also claim them when you file your federal income tax return.

Who is Eligible for Subsidies in 2026?

Eligibility for subsidies primarily hinges on your household income relative to the federal poverty level (FPL) and your household size. While specific income thresholds can vary slightly year to year based on FPL updates, the general guidelines remain consistent.

- Income Requirements: Historically, premium tax credits were available to individuals and families with incomes between 100% and 400% of the FPL. However, recent legislative changes have expanded this, effectively removing the upper income limit and ensuring that no one pays more than 8.5% (or a similar percentage) of their income for a benchmark plan. This critical update means that even if your income is above 400% of the FPL, you might still qualify for significant premium assistance if the cost of coverage exceeds this percentage of your income.

- Household Size: Your household size plays a crucial role in determining your FPL percentage. The larger your household, the higher your income can be while still qualifying for subsidies.

- No Offer of Affordable Employer Coverage: Generally, you won’t be eligible for subsidies through Healthcare.gov if you have an offer of affordable health coverage from an employer. However, there are exceptions. If your employer’s plan is deemed unaffordable (meaning the employee’s share of the premium for self-only coverage exceeds a certain percentage of your household income) or does not meet minimum value standards, you may still qualify for subsidies on the marketplace.

- Citizenship or Lawful Presence: To be eligible, you must be a U.S. citizen or lawfully present in the U.S.

- Not Incarcerated: Individuals who are currently incarcerated are generally not eligible for marketplace plans or subsidies.

Understanding these eligibility criteria is the first step toward maximizing your benefits during the 2026 Healthcare.gov Enrollment. It’s always recommended to use the official Healthcare.gov tools to get an accurate estimate of your eligibility and potential subsidy amounts.

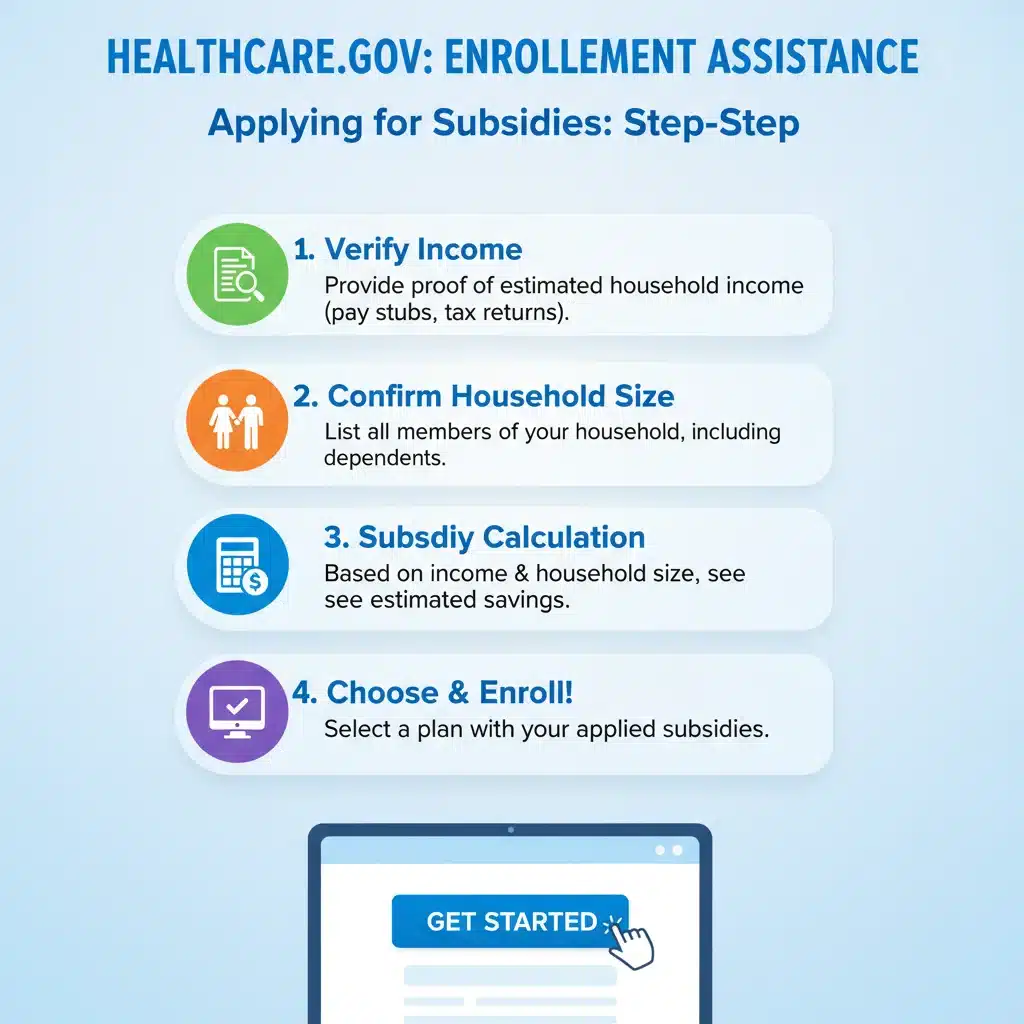

The Step-by-Step Guide to 2026 Healthcare.gov Enrollment

Enrolling in a health insurance plan through Healthcare.gov might seem daunting, but by breaking it down into manageable steps, you can navigate the process with ease. Here’s a comprehensive guide to help you through your 2026 Healthcare.gov Enrollment.

Step 1: Gather Your Information

Before you begin the application, it’s essential to have all necessary documents and information readily available. This will streamline the process and prevent delays.

- Personal Information: Names, dates of birth, Social Security Numbers (SSNs) for everyone in your household applying for coverage.

- Income Information: Estimated adjusted gross income for 2026. This includes wages, salaries, self-employment income, unemployment benefits, Social Security benefits, and any other sources of income. Having recent pay stubs, W-2s, or tax returns can help you estimate accurately.

- Employer Information: If anyone in your household has access to job-based health insurance, you’ll need information about that plan, even if you don’t intend to enroll in it.

- Current Health Insurance Information: Details about any existing health coverage you currently have.

- Immigration Documents: If you are a lawfully present immigrant, you’ll need your immigration document information.

Step 2: Create or Update Your Healthcare.gov Account

If you’re a new user, you’ll need to create an account on Healthcare.gov. If you’ve used the platform before, you can log in to your existing account. It’s crucial to keep your login credentials secure.

Step 3: Complete the Application

The application will ask for details about your household, income, and any current health coverage. Be as accurate as possible, as this information will determine your eligibility for subsidies.

- Household Information: List everyone who will be covered on your plan.

- Income Estimate: Provide your best estimate for your household’s 2026 income. This is critical for subsidy calculations. If your income changes during the year, it’s vital to update your application to avoid issues with tax credits.

- Employer Coverage Questions: Answer truthfully about any job-based health insurance offers.

Step 4: Review Your Eligibility and Explore Plans

Once you submit your application, Healthcare.gov will determine your eligibility for financial assistance, including Premium Tax Credits and Cost-Sharing Reductions. You’ll then be able to browse available plans in your area.

- Plan Categories: Plans are categorized by metal levels: Bronze, Silver, Gold, and Platinum. These levels indicate how you and your plan share costs.

- Bronze: Low monthly premium, high deductible. Good for those who don’t expect to use much medical care.

- Silver: Moderate premium, moderate deductible. If you qualify for CSRs, you must choose a Silver plan to receive them.

- Gold: High monthly premium, low deductible. Good for those who expect to use a lot of medical care.

- Platinum: Highest monthly premium, very low deductible. Offers the most comprehensive coverage.

- Compare Plans: Use the comparison tools on Healthcare.gov to evaluate plans based on premiums, deductibles, out-of-pocket maximums, covered services, and prescription drug formularies. Consider your health needs and financial situation.

Step 5: Select Your Plan and Enroll

After carefully comparing your options, choose the plan that best fits your needs and budget. Once you’ve made your selection, you can proceed to enroll directly through Healthcare.gov. You’ll typically need to make your first premium payment directly to the insurance company to activate your coverage.

Step 6: Confirm Enrollment and Pay Your First Premium

After enrolling, you’ll receive confirmation from Healthcare.gov and your chosen insurance company. It’s crucial to pay your first premium by the due date to ensure your coverage begins as scheduled. Missing this payment can lead to your enrollment being canceled.

Maximizing Your Savings: Strategies for 2026 Healthcare.gov Enrollment

Simply enrolling isn’t enough; smart enrollment involves actively seeking ways to maximize your savings and ensure you’re getting the best value for your healthcare dollars. The 2026 Healthcare.gov Enrollment period offers several opportunities to do just that.

Accurate Income Estimation is Key

Your estimated household income for 2026 is the cornerstone of your subsidy calculation. An accurate estimate can prevent issues down the line.

- Underestimation: If you underestimate your income, you might receive more in advance premium tax credits than you’re eligible for. This could result in owing money back to the IRS when you file your taxes.

- Overestimation: If you overestimate your income, you might receive fewer tax credits than you’re entitled to, meaning you’ll pay higher monthly premiums than necessary. You would then receive the difference as a refund when you file your taxes.

- Update Changes: Life happens. If your income changes significantly during 2026 due to a new job, job loss, marriage, divorce, or other events, update your Healthcare.gov application immediately. This ensures your subsidies are adjusted correctly throughout the year.

Don’t Overlook Cost-Sharing Reductions (CSRs)

If your income qualifies you for CSRs, make sure you choose a Silver-level plan. This is the only way to benefit from these valuable reductions in your deductibles, co-pays, and co-insurance. A Silver plan with CSRs can often provide better overall value than a Gold plan, even with a slightly higher premium, because your out-of-pocket costs will be significantly lower when you use medical services.

Evaluate All Plan Metal Levels

While Silver plans are crucial for CSRs, don’t automatically dismiss Bronze, Gold, or Platinum plans. Your ideal plan depends on your expected healthcare usage:

- Healthy Individuals: A Bronze plan might be suitable if you’re generally healthy and primarily want coverage for catastrophic events, accepting a higher deductible for a lower monthly premium.

- Moderate Healthcare Needs: Silver plans are often a good balance for those with moderate healthcare needs, especially if they qualify for CSRs.

- Frequent Healthcare Users: Gold or Platinum plans might be more cost-effective if you anticipate frequent doctor visits, ongoing prescriptions, or planned surgeries, as they have higher premiums but lower out-of-pocket costs when you receive care.

Consider Your Provider Network

Before finalizing a plan, check if your preferred doctors, specialists, and hospitals are in the plan’s network. Out-of-network care can be significantly more expensive, even with a good insurance plan. Most plans offer online provider search tools.

Review Prescription Drug Coverage

If you take regular prescription medications, confirm that your drugs are covered by the plan’s formulary and understand what tier they fall into. Different tiers have different co-payment or co-insurance amounts.

Seek Local Assistance

Healthcare.gov provides free, local assistance from trained navigators and assisters. These individuals can help you understand your options, complete your application, and enroll in a plan. They are invaluable resources, especially if you have complex circumstances or prefer in-person guidance. You can find local help on the Healthcare.gov website.

Important Dates and Deadlines for 2026 Healthcare.gov Enrollment

Missing deadlines can mean missing out on coverage. While the exact dates for 2026 Healthcare.gov Enrollment will be officially announced closer to the period, based on historical patterns, we can anticipate the general timeline:

- Open Enrollment Period (OEP): Typically, the Open Enrollment Period begins on November 1st and runs through January 15th of the following year. For coverage starting on January 1st, you usually need to enroll by December 15th. Enrolling between December 16th and January 15th means your coverage will likely start on February 1st.

- Special Enrollment Periods (SEPs): Outside of the OEP, you can only enroll in a plan or change your existing plan if you experience a Qualifying Life Event (QLE). QLEs include events such as marriage, birth of a child, loss of other health coverage, moving to a new area, or certain changes in income. Most SEPs allow you 60 days from the date of the QLE to enroll. It’s crucial to report these events promptly to Healthcare.gov.

Always check the official Healthcare.gov website for the most up-to-date and precise dates for the 2026 Healthcare.gov Enrollment period.

Common Questions About 2026 Healthcare.gov Enrollment

Even with detailed guides, questions often arise. Here are answers to some frequently asked questions about 2026 Healthcare.gov Enrollment.

What if my income changes after I enroll?

It is critical to update your income information on your Healthcare.gov account as soon as possible if it changes. This ensures that your premium tax credit is adjusted correctly. If you don’t update it, you could receive too much in subsidies and have to pay it back at tax time, or receive too little and miss out on savings.

Can I get coverage outside of Open Enrollment?

Yes, but only if you qualify for a Special Enrollment Period (SEP). SEPs are triggered by Qualifying Life Events (QLEs) such as getting married, having a baby, losing job-based insurance, or moving to a new area. Without a QLE, you must wait for the next Open Enrollment Period.

What’s the difference between a Premium Tax Credit and a Cost-Sharing Reduction?

A Premium Tax Credit (PTC) lowers your monthly premium payment. A Cost-Sharing Reduction (CSR) lowers your out-of-pocket costs like deductibles, co-payments, and co-insurance. CSRs are only available with Silver plans for those who meet specific income requirements.

Do I have to take the subsidies I’m offered?

No, you are not required to take the advance premium tax credits (APTCs) that are offered. You can choose to pay the full premium yourself and claim the full tax credit when you file your federal income taxes. However, most people opt to receive the APTCs to lower their monthly payments.

What if I don’t qualify for subsidies?

Even if you don’t qualify for subsidies, you can still purchase a health insurance plan through Healthcare.gov. The marketplace offers a variety of plans from different insurance companies, allowing you to compare options and find a plan that meets your needs directly. You can also explore options outside the marketplace, but those plans typically do not come with federal subsidies.

How do I choose the right plan?

Choosing the right plan involves considering several factors:

- Your health needs: How often do you visit the doctor? Do you have chronic conditions or take regular medications?

- Your budget: What can you afford for monthly premiums and potential out-of-pocket costs?

- Your preferred providers: Are your doctors and hospitals in the plan’s network?

- Plan metal level: Bronze, Silver, Gold, or Platinum, each offering different cost-sharing structures.

Use the comparison tools on Healthcare.gov and consider seeking assistance from a navigator if you’re unsure.

The Future of Healthcare Access and Affordability

The continuous evolution of the Affordable Care Act and the enhancements to subsidies underscore a commitment to making healthcare accessible and affordable for all Americans. The 2026 Healthcare.gov Enrollment period is a critical juncture for millions to secure vital health coverage with potentially significant financial assistance.

The ongoing adjustments to the ACA, particularly around subsidy structures, reflect a dynamic response to the economic realities and healthcare needs of the population. By understanding these changes, actively engaging with the enrollment process, and leveraging the available resources, individuals and families can navigate the marketplace effectively. The goal remains to reduce the number of uninsured individuals and ensure that financial barriers do not prevent access to necessary medical care.

As you prepare for 2026 Healthcare.gov Enrollment, remember that accurate information, timely action, and a clear understanding of your options are your most powerful tools. Don’t hesitate to utilize the free resources provided by Healthcare.gov, including their website, call center, and local assistance programs. These resources are designed to help you make the best decisions for your health and financial well-being.

Conclusion: Empowering Your 2026 Healthcare.gov Enrollment Journey

The 2026 Healthcare.gov Enrollment period presents a significant opportunity for millions of Americans to secure affordable health insurance coverage. With the anticipated continuation and potential enhancement of subsidies, more individuals and families than ever before may find themselves eligible for financial assistance that dramatically reduces the cost of their premiums and out-of-pocket expenses.

By following this comprehensive guide, you are now equipped with the knowledge to understand the new subsidy landscape, determine your eligibility, and navigate the step-by-step enrollment process with confidence. Remember to gather all necessary information, accurately estimate your income, compare plans diligently, and stay informed about important dates and deadlines.

Healthcare is a fundamental right, and the mechanisms provided through Healthcare.gov, particularly the robust subsidy programs, are designed to make that right a reality for more people. Take the time to explore your options, ask questions, and utilize the available resources. Your proactive approach to 2026 Healthcare.gov Enrollment will not only secure your health coverage but also empower you with greater financial stability and peace of mind. Make the most of this opportunity to invest in your health and future.