Navigating 2026 Federal Loan Forgiveness: Your Guide to Student Debt Relief

Anúncios

Navigating 2026 Federal Loan Forgiveness: Your Definitive Guide to Student Debt Relief

The burden of student loan debt is a significant concern for millions across the United States. As we look towards 2026, understanding the nuances of Federal Loan Forgiveness 2026 programs becomes paramount for those seeking relief. The landscape of federal student aid and repayment options is constantly evolving, making it crucial for borrowers to stay informed about the latest policies and potential opportunities for debt cancellation. This comprehensive guide aims to demystify the various federal loan forgiveness programs available in 2026, helping you determine which options might be best suited for your financial situation and how to navigate the application process effectively.

Anúncios

Student loan debt can impact every aspect of a borrower’s life, from career choices to major life milestones like buying a home or starting a family. Fortunately, the U.S. Department of Education offers several programs designed to provide relief, ranging from forgiveness for public service workers to options based on income and disability. However, these programs often come with specific eligibility requirements, application processes, and timelines that can be complex to understand. By providing a detailed overview of Federal Loan Forgiveness 2026, we hope to empower you with the knowledge needed to make informed decisions about your student debt.

The year 2026 is a critical juncture for many borrowers, as some programs might see adjustments, while others continue to offer substantial relief. Whether you are currently enrolled in a repayment plan, considering your options, or simply looking ahead, this article will serve as your essential resource. We will delve into the specifics of each major federal student loan forgiveness program, outline their benefits and drawbacks, and offer practical advice on how to maximize your chances of approval. Our goal is to simplify the complex world of student loan forgiveness, making it accessible and actionable for every borrower.

Anúncios

Understanding the Basics of Federal Loan Forgiveness 2026

Before diving into specific programs, it’s essential to grasp the fundamental principles behind Federal Loan Forgiveness 2026. Federal loan forgiveness, cancellation, or discharge refers to the elimination of some or all of a borrower’s remaining student loan balance. This is distinct from deferment or forbearance, which only temporarily pause payments. Forgiveness is typically granted under specific circumstances, often tied to a borrower’s profession, income, or certain life events.

It’s important to distinguish between federal student loans and private student loans. Federal loan forgiveness programs exclusively apply to federal student loans (e.g., Direct Loans, FFEL Program loans, Perkins Loans). Private student loans, issued by banks or other private lenders, generally do not qualify for these federal programs, though some private lenders may offer their own limited relief options. Therefore, the first step in exploring Federal Loan Forgiveness 2026 is to confirm that you hold federal student loans.

Another crucial aspect is the tax implications of forgiveness. While many federal loan forgiveness programs offer tax-free forgiveness, some types of debt cancellation might be considered taxable income by the IRS. It’s always advisable to consult with a tax professional to understand the potential tax consequences of any forgiven debt, especially as tax laws can change. Staying informed about these foundational elements will help you navigate the more detailed aspects of each program.

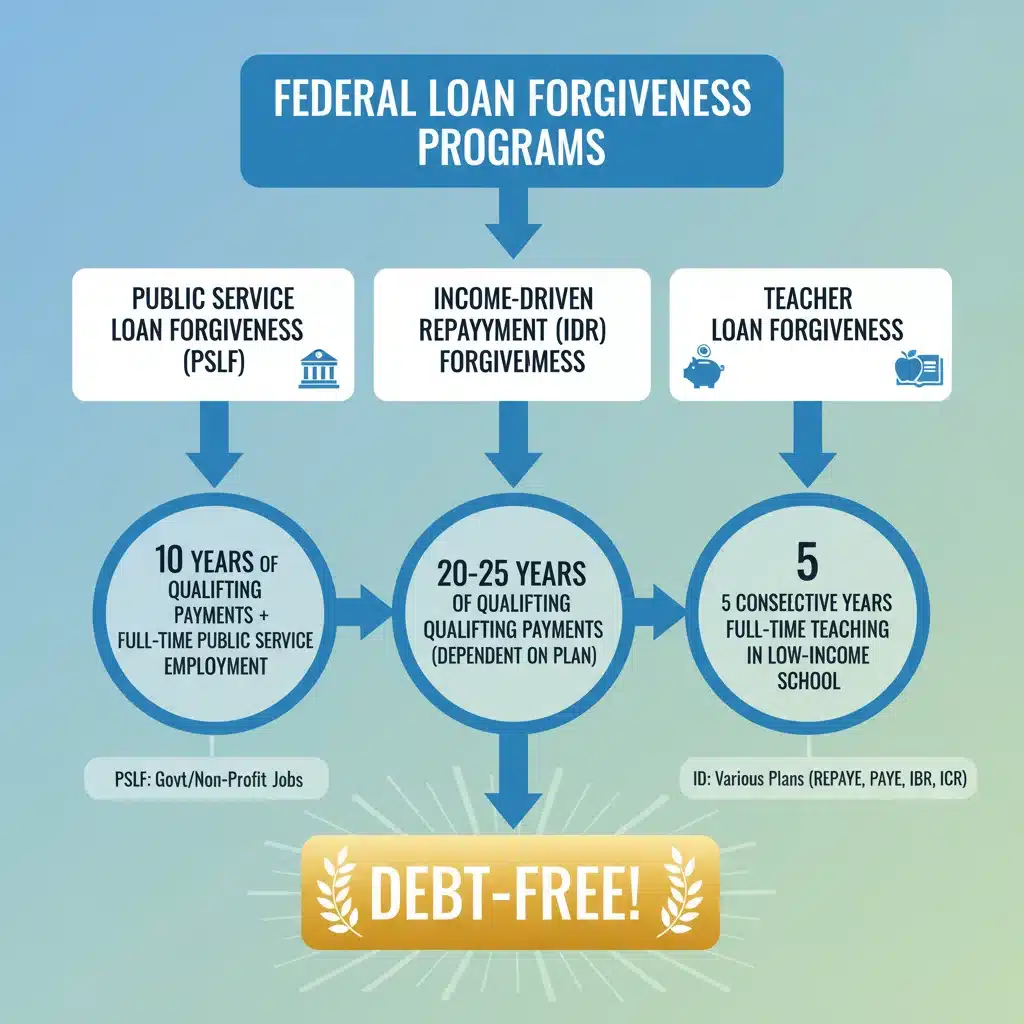

Public Service Loan Forgiveness (PSLF) in 2026

The Public Service Loan Forgiveness (PSLF) program remains one of the most significant pathways to debt relief for those working in public service. As of 2026, PSLF continues to offer tax-free forgiveness of the remaining balance on Direct Loans after 120 qualifying payments (10 years) have been made under a qualifying repayment plan while working full-time for a qualifying employer. This program is a cornerstone of Federal Loan Forgiveness 2026 for many dedicated professionals.

Who Qualifies for PSLF?

To be eligible for PSLF, borrowers must meet several criteria:

- Employment: You must be employed full-time by a U.S. federal, state, local, or tribal government organization, or a non-profit organization that is tax-exempt under Section 501(c)(3) of the Internal Revenue Code. Certain other non-profit organizations that provide specific public services may also qualify.

- Loan Type: Only Direct Loans are eligible. If you have FFEL Program loans or Perkins Loans, you may need to consolidate them into a Direct Consolidation Loan to qualify.

- Repayment Plan: You must make 120 qualifying monthly payments under a qualifying income-driven repayment (IDR) plan. These plans include Revised Pay As You Earn (REPAYE), Pay As You Earn (PAYE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). Payments made under the Standard Repayment Plan also count if they are made while on a qualifying employment, but only for the 10-year period, after which your loans would already be paid off.

- Payment Requirements: Payments must be made on time, for the full amount due, and after October 1, 2007.

Optimizing Your PSLF Journey for 2026

For borrowers pursuing PSLF, consistent tracking and annual certification are vital. The PSLF Help Tool on StudentAid.gov allows you to search for qualifying employers and submit your Employment Certification Form (ECF) annually or whenever you change employers. This ensures that your employment and payments are being correctly counted towards the 120 required payments. Neglecting this step can lead to delays or issues when applying for forgiveness.

Staying on a qualifying income-driven repayment plan is also critical. Your monthly payment amount under an IDR plan is calculated based on your income and family size, which can result in lower payments, especially for those with modest incomes relative to their debt. This makes the remaining balance larger at the end of the 10 years, maximizing the benefit of PSLF. As we move into 2026, be aware of any potential updates or changes to IDR plan rules that might impact your PSLF eligibility or payment amounts.

Income-Driven Repayment (IDR) Plan Forgiveness in 2026

Beyond PSLF, Income-Driven Repayment (IDR) plans themselves offer a path to forgiveness for borrowers who do not work in public service. These plans are designed to make loan payments more manageable by capping them at a percentage of your discretionary income. Any remaining balance after a specified repayment period (typically 20 or 25 years, depending on the plan and when you borrowed) is forgiven. This is another critical component of Federal Loan Forgiveness 2026.

Types of IDR Plans

There are four main IDR plans:

- Revised Pay As You Earn (REPAYE) Plan: Generally 10% of discretionary income. Forgiveness after 20 years for undergraduate loans, 25 years for graduate loans.

- Pay As You Earn (PAYE) Plan: Generally 10% of discretionary income, but never more than the 10-year Standard Repayment Plan amount. Forgiveness after 20 years.

- Income-Based Repayment (IBR) Plan: Generally 10% or 15% of discretionary income, depending on when you borrowed. Forgiveness after 20 or 25 years.

- Income-Contingent Repayment (ICR) Plan: The lesser of 20% of discretionary income or what you’d pay on a fixed 12-year plan. Forgiveness after 25 years.

The New SAVE Plan (formerly REPAYE) and Its Impact on 2026 Forgiveness

A significant development impacting Federal Loan Forgiveness 2026 is the implementation of the new Saving on a Valuable Education (SAVE) Plan, which replaces the REPAYE plan. The SAVE Plan offers several enhancements designed to lower monthly payments and accelerate forgiveness for many borrowers. Key features include:

- Lower Discretionary Income Calculation: The SAVE Plan increases the income exemption from 150% to 225% of the federal poverty line, meaning more of your income is protected and not factored into your payment calculation.

- Elimination of Unpaid Interest Accumulation: If your monthly payment is less than the interest that accrues, the government covers the remaining interest. This prevents your loan balance from growing, a common issue under other IDR plans.

- Shorter Forgiveness Timelines for Small Balances: Forgiveness could be granted in as little as 10 years for borrowers with original principal balances of $12,000 or less, with an additional year added for every $1,000 borrowed above that amount, up to the standard 20 or 25 years.

These changes under the SAVE plan are particularly impactful for borrowers with lower incomes and smaller loan balances, offering a potentially faster route to forgiveness by 2026 and beyond. It is highly recommended that borrowers review their eligibility for the SAVE Plan and consider enrolling if it offers a better path to managing their debt and achieving forgiveness.

Teacher Loan Forgiveness Programs in 2026

Educators play a vital role in our communities, and several programs are specifically designed to offer them relief. The Teacher Loan Forgiveness (TLF) program is one such option, providing up to $17,500 in forgiveness for eligible teachers. This program complements other Federal Loan Forgiveness 2026 initiatives by targeting a specific professional group.

Eligibility for Teacher Loan Forgiveness

To qualify for TLF:

- You must have Direct Subsidized or Unsubsidized Loans, or FFEL Program loans.

- You must teach full-time for five complete and consecutive academic years in a low-income elementary or secondary school or educational service agency.

- The loan(s) for which you are seeking forgiveness must have been made before the end of your five years of qualifying teaching service.

Forgiveness Amounts

The amount of forgiveness you can receive depends on your teaching subject:

- Up to $17,500: Available for highly qualified full-time math, science, or special education teachers at the secondary level, or elementary school teachers who demonstrate expertise in reading instruction and teach in eligible low-income schools.

- Up to $5,000: Available for other highly qualified full-time elementary and secondary school teachers who teach in eligible low-income schools.

It’s important to note that the five years of service for TLF do not count towards the 120 payments required for PSLF. You cannot receive forgiveness for the same period of service under both programs. Teachers should carefully evaluate which program offers the most significant benefit based on their loan balance, income, and career trajectory.

Total and Permanent Disability (TPD) Discharge

For borrowers facing severe health challenges, the Total and Permanent Disability (TPD) discharge offers a complete cancellation of federal student loans. This is a crucial safety net within the framework of Federal Loan Forgiveness 2026, providing relief to those unable to work due to a disability.

How to Qualify for TPD Discharge

You can qualify for TPD discharge in one of three ways:

- Veterans Affairs (VA) Determination: If the VA determines that you have a service-connected disability that is 100% disabling or you are totally disabled based on an individual unemployability rating.

- Social Security Administration (SSA) Determination: If you receive Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI) benefits, and your notice of award states that your next review will be 5 to 7 years or more from the date of your last review.

- Physician’s Certification: A physician certifies that you are unable to engage in any substantial gainful activity due to a physical or mental impairment that can be expected to result in death, has lasted for a continuous period of at least 60 months, or can be expected to last for a continuous period of at least 60 months.

Once approved for TPD discharge, there is typically a three-year post-discharge monitoring period. During this period, you must not earn income exceeding the poverty guideline for a family of two, or receive new federal student loans or TEACH Grant service obligations. If you meet these conditions, your loans will remain discharged. This program offers significant relief for those who meet the strict disability criteria, providing a pathway to being debt-free.

Other Specific Forgiveness and Discharge Programs

Beyond the major programs, several other specific circumstances can lead to federal student loan forgiveness or discharge. These are important considerations for Federal Loan Forgiveness 2026, catering to unique situations:

Borrower Defense to Repayment

This program offers loan discharge if your school misled you or engaged in other misconduct in violation of certain state laws. This typically applies to cases where schools made false promises about job placement, accreditation, or the quality of their education. The process involves submitting an application to the Department of Education, providing evidence of the school’s misconduct. The rules and processing of these claims have seen significant changes over the years, and borrowers should check the latest guidelines on StudentAid.gov.

Closed School Discharge

If your school closes while you are enrolled or soon after you withdraw, and you don’t complete your program at another school or through a teach-out agreement, you may be eligible for a closed school discharge. This cancels 100% of your federal student loans borrowed to attend that specific school. This is a crucial protection for students whose educational path is disrupted by institutional failure.

False Certification Discharge

You might qualify for a false certification discharge if your school falsely certified your eligibility to receive federal student loans. This can occur if the school falsely certified your ability to benefit from the education, or if it forged your signature on application materials, or if your identity was stolen and used to obtain loans.

Death Discharge

In the unfortunate event of a borrower’s death, federal student loans are discharged upon receipt of a death certificate. This ensures that student loan debt is not passed on to heirs or family members, providing peace of mind during a difficult time.

Strategizing for Federal Loan Forgiveness 2026: What You Need to Do Now

Navigating the various Federal Loan Forgiveness 2026 programs can be complex, but strategic planning can significantly improve your chances of success. Here are key steps to take:

1. Understand Your Loan Types

The first and most critical step is to know what type of federal student loans you have. Log in to StudentAid.gov to view your loan history, current servicer, and loan types. This information will dictate which forgiveness programs you are eligible for. If you have FFEL or Perkins loans, consider consolidation into a Direct Consolidation Loan to open up eligibility for PSLF and most IDR plans.

2. Assess Your Eligibility for PSLF

If you work in public service, regularly use the PSLF Help Tool to confirm your employer’s eligibility and submit your Employment Certification Form (ECF) annually. This proactive approach helps track your qualifying payments and identify any issues early on. Ensure you are enrolled in a qualifying IDR plan to maximize your forgiveness potential.

3. Explore Income-Driven Repayment Plans, Especially SAVE

For all federal loan borrowers, especially those with high debt-to-income ratios, an IDR plan can significantly lower your monthly payments. The new SAVE Plan offers the most generous terms for many, particularly by preventing interest capitalization and offering shorter forgiveness timelines for smaller balances. Recertify your income and family size annually to ensure your payments remain accurate and affordable.

4. Stay Informed About Policy Changes

The landscape of student loan policy is dynamic. Keep an eye on announcements from the U.S. Department of Education and reliable financial news sources. Changes to IDR plans, PSLF rules, or the introduction of new forgiveness initiatives could impact your strategy for Federal Loan Forgiveness 2026. Subscribing to updates from StudentAid.gov is an excellent way to stay informed.

5. Maintain Meticulous Records

For any forgiveness program, especially PSLF, maintaining thorough records is essential. Keep copies of your loan statements, payment confirmations, employment certification forms, and any correspondence with your loan servicer. This documentation can be invaluable if disputes arise regarding your eligibility or payment count.

6. Seek Professional Guidance If Needed

If you find the process overwhelming or have a particularly complex situation, consider consulting with a non-profit student loan counselor or a financial advisor specializing in student debt. They can offer personalized advice and help you navigate the intricacies of Federal Loan Forgiveness 2026 programs.

Common Pitfalls to Avoid When Pursuing Forgiveness

While federal loan forgiveness offers significant relief, there are common mistakes borrowers make that can jeopardize their eligibility or delay the process. Being aware of these pitfalls is just as important as understanding the programs themselves when pursuing Federal Loan Forgiveness 2026.

1. Not Consolidating the Right Loans

Many borrowers with older FFEL Program loans or Perkins Loans fail to consolidate them into a Direct Consolidation Loan, which is a prerequisite for PSLF and some IDR plans. Without consolidation, these loans will never qualify for these specific federal forgiveness programs. It’s crucial to understand that consolidation creates a new Direct Loan, and in some cases, can reset your payment count for PSLF, though recent waivers have offered temporary relief to address this for some borrowers. Always check the latest guidance before consolidating.

2. Incorrect Repayment Plan Enrollment

For PSLF, only payments made under an income-driven repayment plan or the Standard Repayment Plan (for the 10-year period) count. Making payments under an Extended Repayment Plan or Graduated Repayment Plan will not count towards the 120 required payments. Ensure you are on the correct plan and that your servicer has accurately recorded it.

3. Failing to Certify Employment Annually for PSLF

Even if you’re confident in your employer’s eligibility, not submitting the Employment Certification Form (ECF) annually or when you change jobs can lead to issues. This form allows the Department of Education to track your progress and confirm your qualifying employment. Without regular certification, you might find discrepancies in your payment count when you finally apply for forgiveness, causing significant delays.

4. Missing Annual IDR Recertification

Borrowers on IDR plans must recertify their income and family size annually. Failing to do so can result in your payments reverting to the higher Standard Repayment amount, or interest capitalization, leading to a larger loan balance. This can also disrupt your progress towards IDR forgiveness. Always mark your calendar for your recertification deadline.

5. Not Understanding Tax Implications

While PSLF and TPD discharge are generally tax-free, forgiveness under IDR plans (after 20 or 25 years) may be considered taxable income by the IRS. This could lead to a significant tax bill in the year your loans are forgiven. It’s vital to plan for this potential tax liability by consulting with a tax professional and potentially setting aside funds.

6. Falling Victim to Scams

Be wary of companies that promise quick or guaranteed student loan forgiveness for a fee. These are often scams. All federal student loan forgiveness programs are free to apply for through your loan servicer or StudentAid.gov. Never pay for services you can get for free.

By diligently avoiding these common pitfalls, you can significantly streamline your journey towards Federal Loan Forgiveness 2026 and ensure you receive the relief you are entitled to.

The Future of Federal Loan Forgiveness Beyond 2026

The landscape of federal student loan policy is subject to ongoing review and potential reform. While we’ve focused on Federal Loan Forgiveness 2026, it’s important for borrowers to remain aware that future changes could impact existing programs or introduce new opportunities for relief. Legislative actions, executive orders, and regulatory adjustments can all shape the availability and terms of loan forgiveness.

For example, there have been ongoing discussions about broader student loan cancellation initiatives, although the path for such comprehensive programs remains uncertain. The Department of Education continues to refine existing programs, as seen with the introduction of the SAVE plan, and may make further adjustments to improve efficiency or expand access to relief. Staying engaged with official government resources and reputable news outlets will be key to understanding how these potential future developments might affect your student loan strategy.

Planning for your financial future means not only understanding the current opportunities but also being prepared for potential shifts. Regularly reviewing your loan status, repayment plan, and eligibility for various programs ensures that you can adapt to any new policies and continue on the most advantageous path toward managing and ultimately eliminating your student debt.

Conclusion: Charting Your Course to Debt Relief with Federal Loan Forgiveness 2026

Navigating the complex world of federal student loan forgiveness requires diligence, understanding, and proactive engagement. As we’ve explored, Federal Loan Forgiveness 2026 offers several distinct pathways to debt relief, each with its own set of eligibility criteria and benefits. From the dedicated public servant pursuing PSLF to the borrower benefiting from the new SAVE plan’s generous terms, opportunities exist to significantly reduce or eliminate your student loan burden.

The key takeaways for any borrower are to:

- Identify Your Loan Types: This is the foundational step for determining eligibility.

- Research All Available Programs: Don’t assume one program is your only option; explore PSLF, IDR forgiveness (especially SAVE), Teacher Loan Forgiveness, and disability discharges.

- Act Proactively: Certify employment, recertify income, and submit applications on time.

- Maintain Records: Keep meticulous documentation of everything related to your loans.

- Stay Informed: Policy changes can impact your eligibility and strategy.

By taking these steps, you can confidently chart your course toward financial freedom from student debt. The information provided in this guide serves as a powerful tool to help you understand the landscape of Federal Loan Forgiveness 2026. Remember, you don’t have to face your student loans alone. Utilize the resources available, seek professional advice if necessary, and take control of your financial future. The path to debt relief is within reach for informed and proactive borrowers.