2026 First-Time Homebuyer Programs: Federal Aid & Opportunities

Anúncios

Alert: New 2026 Federal Programs for First-Time Homebuyers – Don’t Miss These Opportunities

The dream of homeownership remains a cornerstone of the American ideal, yet for many first-time homebuyers, it often feels like an insurmountable challenge. The complexities of saving for a down payment, navigating mortgage options, and understanding eligibility requirements can be daunting. However, the landscape for aspiring homeowners is continually evolving, and 2026 is poised to bring significant new opportunities through updated federal programs designed specifically to ease the path to homeownership for first-time buyers. This comprehensive guide will delve into these crucial First-Time Homebuyer Programs, highlighting what’s new, what’s changing, and how you can position yourself to take full advantage of these invaluable resources.

Anúncios

Understanding the various federal initiatives is the first step toward unlocking your homeownership potential. These programs are not merely abstract government policies; they are tangible tools, offering everything from down payment assistance and closing cost support to favorable loan terms and interest rate reductions. For first-time homebuyers, these programs can be the difference between renting indefinitely and finally owning a place to call their own. As we look towards 2026, several key federal agencies are refining and introducing new provisions to make homeownership more accessible and affordable than ever before.

The Evolving Landscape of Federal First-Time Homebuyer Programs in 2026

The federal government plays a pivotal role in supporting the housing market, particularly for those entering it for the first time. In 2026, we anticipate several enhancements and new initiatives within existing programs, alongside potential entirely new offerings. These updates are often driven by economic conditions, housing market trends, and a commitment to equitable access to homeownership. The primary goal remains consistent: to reduce the financial barriers that often prevent first-time buyers from purchasing a home.

Anúncios

Key Agencies and Their Contributions

Several federal departments and agencies are central to providing First-Time Homebuyer Programs. Understanding their roles is crucial:

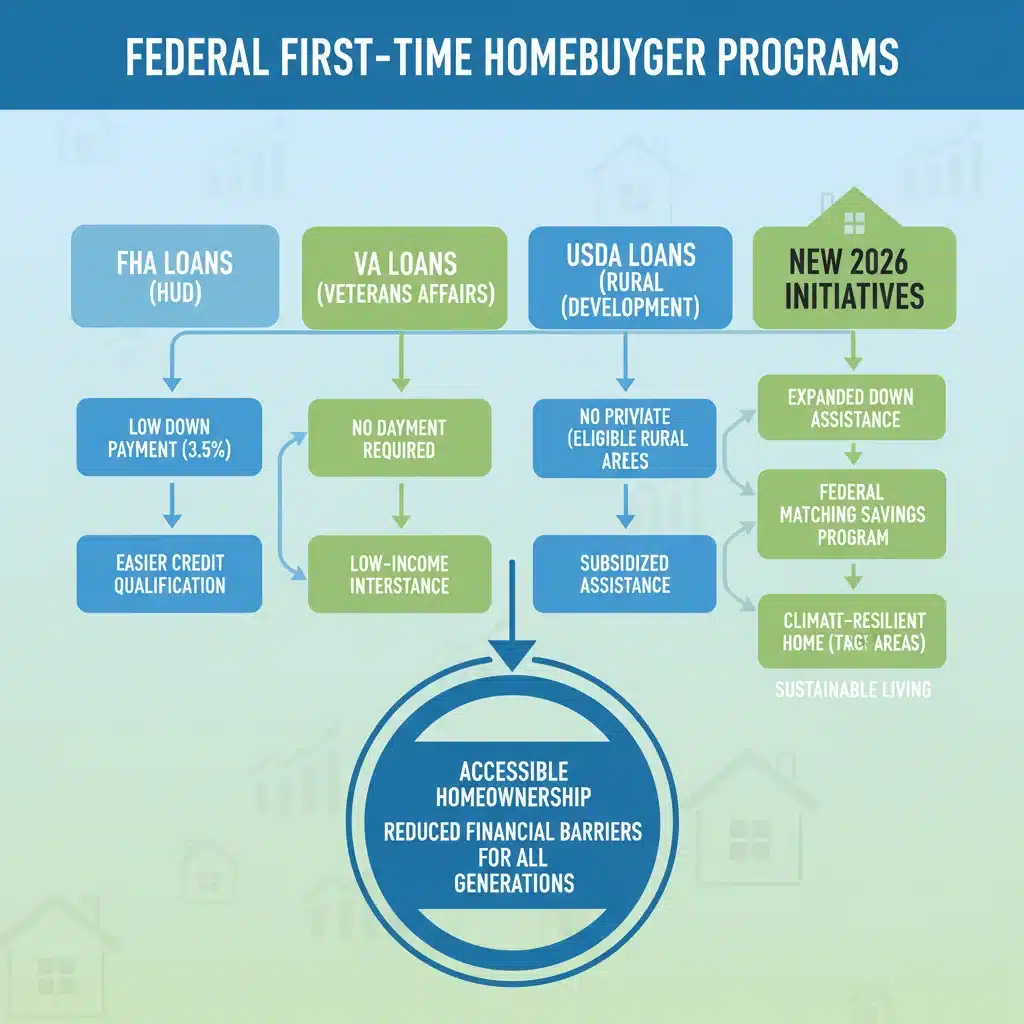

- Federal Housing Administration (FHA): A long-standing pillar of support, the FHA insures mortgages issued by approved lenders. This insurance protects lenders from losses if a borrower defaults, making them more willing to offer loans to borrowers who might not qualify for conventional mortgages. FHA loans are particularly attractive to first-time buyers due to their lower down payment requirements (as little as 3.5%) and more flexible credit score criteria.

- U.S. Department of Veterans Affairs (VA): The VA loan program is an incredible benefit for eligible service members, veterans, and surviving spouses. It offers the unparalleled advantage of 0% down payment and often requires no private mortgage insurance (PMI). These loans are guaranteed by the VA, reducing risk for lenders.

- U.S. Department of Agriculture (USDA): The USDA Rural Development program offers loans to low- and moderate-income individuals in eligible rural areas. Similar to VA loans, USDA loans often require no down payment, making them a fantastic option for those looking to buy outside of densely populated urban centers.

- Fannie Mae and Freddie Mac: While not direct lenders, these government-sponsored enterprises (GSEs) play a massive role in the mortgage market by purchasing loans from lenders, thereby providing liquidity. They also set guidelines for conventional loans and offer specific programs, such as Fannie Mae’s HomeReady and Freddie Mac’s Home Possible, which are designed for low- to moderate-income borrowers and often feature lower down payment options and flexible credit requirements.

Anticipated Changes and New Initiatives for 2026

While specific legislative details are always subject to change, discussions and proposals frequently revolve around enhancing existing programs and introducing new ones. For 2026, potential updates to First-Time Homebuyer Programs could include:

- Increased Down Payment Assistance: Expect a continued focus on programs that provide grants or forgivable loans for down payments and closing costs. These are often administered at the state or local level but receive federal funding or incentives. New federal matching programs could encourage more local participation.

- Expanded Eligibility Criteria: Some proposals aim to broaden the income and credit score ranges for certain federal loans, allowing a larger segment of the population to qualify. This could mean more flexible underwriting standards for FHA or GSE-backed loans.

- Focus on Affordable Housing Supply: Beyond just financing, federal efforts might increasingly support initiatives to boost the supply of affordable housing, which indirectly benefits first-time buyers by stabilizing or lowering home prices in certain markets.

- Energy Efficiency Incentives: There’s a growing trend towards incentivizing energy-efficient home purchases. New federal programs might offer grants or tax credits for first-time buyers who purchase or renovate homes to meet certain energy efficiency standards, reducing long-term ownership costs.

- Targeted Programs for Underserved Communities: Federal programs are increasingly looking to address historical disparities in homeownership. Expect new or enhanced initiatives aimed at providing extra support and resources to historically marginalized groups and communities.

Decoding the Benefits: Why These Programs Matter for First-Time Homebuyers

The benefits of federal First-Time Homebuyer Programs are multifaceted and directly address the most common hurdles faced by aspiring homeowners. Understanding these advantages is key to determining which program best suits your needs.

Lower Down Payments

One of the biggest obstacles for first-time buyers is accumulating a substantial down payment. Conventional loans often require 10-20% of the home’s purchase price, which for a $300,000 home, means $30,000 to $60,000. Federal programs drastically reduce this burden:

- FHA Loans: As low as 3.5% down.

- VA and USDA Loans: Often 0% down for eligible borrowers and properties.

- GSE Programs (HomeReady, Home Possible): As low as 3% down.

These lower requirements make homeownership attainable much sooner, allowing buyers to enter the market without years of aggressive saving.

More Flexible Credit Requirements

Excellent credit is not a prerequisite for all federal loan programs. While a strong credit score always helps, many federal options are more forgiving:

- FHA Loans: Generally accept credit scores as low as 580 for the 3.5% down payment, and even lower (500-579) with a 10% down payment.

- VA and USDA Loans: Do not set a minimum credit score, though lenders will have their own requirements, typically around 620-640. The federal guarantee makes lenders more flexible.

This flexibility opens doors for individuals who may have had past credit challenges but are now financially stable.

Reduced Closing Costs

Beyond the down payment, closing costs—which include appraisal fees, title insurance, attorney fees, and more—can add another 2-5% to the home’s price. Some federal programs and related state/local initiatives offer assistance with these costs, either through grants, seller concessions, or by allowing them to be rolled into the loan.

Lower Interest Rates

Federal backing often translates to more competitive interest rates. Because the government insures or guarantees a portion of the loan, lenders perceive less risk, which can lead to lower rates for borrowers. Even a small reduction in interest rate can save tens of thousands of dollars over the life of a 30-year mortgage.

No Private Mortgage Insurance (PMI) for Some Loans

For conventional loans with less than 20% down, borrowers typically pay PMI, an additional monthly cost that protects the lender. VA loans famously require no PMI. FHA loans have mortgage insurance premiums (MIP) that function similarly but are structured differently. Understanding these nuances is important for calculating your total monthly housing expense.

Navigating the Application Process: Your Roadmap to Homeownership

While the benefits are clear, successfully securing a federal loan requires careful preparation and understanding of the application process. Here’s a step-by-step guide for first-time homebuyers:

Step 1: Assess Your Financial Health

Before even looking at homes, get your finances in order. This includes:

- Checking Your Credit Score: Obtain your credit report from all three major bureaus (Experian, Equifax, TransUnion) and dispute any errors. Work on improving your score if necessary by paying down debt and making payments on time.

- Calculating Your Debt-to-Income (DTI) Ratio: Lenders look at how much of your gross monthly income goes towards debt payments. Most federal programs have DTI limits (e.g., FHA typically allows up to 43-50%).

- Estimating Your Budget: Beyond the mortgage payment, factor in property taxes, homeowner’s insurance, potential HOA fees, and maintenance costs.

- Saving for a Down Payment and Closing Costs: Even with low-down-payment options, having some savings is crucial. Explore down payment assistance programs available in your state or locality, which often stack with federal loans.

Step 2: Get Pre-Approved for a Mortgage

Pre-approval is a critical step that demonstrates to sellers that you are a serious and qualified buyer. It involves a lender reviewing your financial information to determine how much they are willing to lend you. This is also where you’ll explore which federal First-Time Homebuyer Programs you qualify for.

- Find a Lender: Look for lenders experienced with FHA, VA, USDA, or other federal programs. Not all lenders offer all types of loans.

- Gather Documentation: Be prepared to provide pay stubs, W-2s, tax returns, bank statements, and other financial records.

- Understand Your Options: A good lender will explain the different federal loan programs, their specific requirements, and which one is the best fit for your situation.

Step 3: Find Your Dream Home

With pre-approval in hand, you can confidently begin your home search. Work with a real estate agent who understands the nuances of federal loan programs, as some properties may have specific requirements (e.g., USDA loans require properties in designated rural areas, FHA loans have minimum property standards).

Step 4: Make an Offer and Undergo Appraisal/Inspection

Once you find a home, your agent will help you make an offer. After an offer is accepted, the process will involve:

- Home Inspection: Highly recommended to identify any potential issues with the property.

- Appraisal: Required by lenders to ensure the home’s value supports the loan amount. Federal loans, especially FHA and VA, have specific appraisal requirements to ensure the home is safe, sound, and sanitary.

Step 5: Final Underwriting and Closing

The lender will finalize their review of your finances and the property. Once approved, you’ll proceed to closing, where you’ll sign all necessary documents and officially become a homeowner. This is where all the benefits of the federal First-Time Homebuyer Programs come to fruition.

Beyond Federal: State and Local First-Time Homebuyer Programs

It’s important to remember that federal programs often work in conjunction with state and local initiatives. Many states, counties, and cities offer their own First-Time Homebuyer Programs, which can include:

- Down Payment Assistance (DPA) Programs: These often come as grants, deferred loans, or low-interest loans that can be combined with federal mortgages.

- First-Time Homebuyer Tax Credits: Some states offer tax credits that can provide significant savings.

- Mortgage Credit Certificates (MCCs): These allow qualified homeowners to claim a tax credit for a portion of the mortgage interest paid each year.

- Homebuyer Education and Counseling: Many programs require or strongly recommend first-time buyer education, which provides invaluable knowledge about the homeownership process.

Always research what programs are available in your specific area, as they can significantly enhance the benefits of federal loans.

Common Misconceptions About First-Time Homebuyer Programs

Despite their widespread availability, several myths persist about First-Time Homebuyer Programs that can deter potential applicants. Let’s debunk some of the most common ones:

Myth 1: You need perfect credit to qualify.

Reality: As discussed, many federal programs, particularly FHA and VA, are designed for borrowers with less-than-perfect credit scores. While a higher score is always beneficial, it’s not a deal-breaker for these programs.

Myth 2: These programs are only for low-income individuals.

Reality: While some programs have income limits (like USDA loans), many, such as FHA and VA, do not have strict income caps. Their primary focus is on making homeownership accessible, not exclusively for the lowest income brackets. Eligibility often depends on a combination of factors, not just income.

Myth 3: The application process is overly complicated and takes too long.

Reality: While buying a home involves paperwork, the process for federal loans is streamlined and well-established. With the help of an experienced lender and real estate agent, it can be as straightforward as a conventional loan. The benefits often far outweigh any perceived complexity.

Myth 4: These programs are only for buying specific types of homes.

Reality: While some programs have property-specific requirements (e.g., USDA for rural areas), most federal loans can be used for a wide range of property types, including single-family homes, condos, and even some multi-family properties, provided they meet program standards.

Myth 5: You can only use these programs once.

Reality: Most First-Time Homebuyer Programs are indeed designed for first-time buyers. However, the definition of a ‘first-time homebuyer’ can be broader than you think. It often includes individuals who haven’t owned a home in the past three years. Additionally, programs like VA loans can be used multiple times by eligible veterans.

Preparing for 2026: What You Can Do Now

If you’re eyeing homeownership in 2026, there are several proactive steps you can take today to ensure you’re ready to seize the opportunities presented by new and updated federal programs:

- Educate Yourself: Continuously research and stay informed about potential legislative changes and program updates. Follow housing news from government agencies and reputable financial outlets.

- Improve Your Credit: Start building or repairing your credit score now. Pay bills on time, reduce credit card debt, and avoid opening new lines of credit unnecessarily.

- Save Diligently: Even if you plan to use a low-down-payment loan, having a financial cushion for closing costs, initial repairs, or emergencies is wise. Set up an automatic savings plan.

- Reduce Debt: Lowering your overall debt, especially high-interest consumer debt, will improve your debt-to-income ratio and make you a more attractive borrower.

- Attend Homebuyer Education Courses: Many non-profit organizations offer free or low-cost homebuyer education. These courses provide invaluable insights into the entire home-buying process and can be a requirement for some DPA programs.

- Consult a Housing Counselor: HUD-approved housing counselors can provide personalized advice and help you navigate the various programs available.

- Connect with a Lender: Start talking to lenders who specialize in federal loans well in advance. They can provide tailored advice on what you need to do to qualify for First-Time Homebuyer Programs in 2026.

The Future of Homeownership for First-Time Buyers

The federal government’s commitment to supporting first-time homebuyers is a continuous effort, and the 2026 landscape promises to be one of evolving support and expanded opportunities. While the housing market can present its challenges, the existence of robust First-Time Homebuyer Programs ensures that the path to owning a home remains accessible for millions of Americans.

By staying informed, preparing your finances, and leveraging the expert advice of lenders and real estate professionals, you can confidently navigate the home-buying journey. Don’t let the complexities deter you; instead, view them as steps on a clear path. The dream of owning your own home is within reach, and with the right strategy and the assistance of federal programs, 2026 could be the year you turn that dream into a reality. Start your preparation today, and be ready to unlock the doors to your new home when these exciting new opportunities arrive.

Remember, the key is proactive engagement. The sooner you understand the requirements and begin to align your financial situation with them, the better positioned you will be to capitalize on the benefits offered by the 2026 First-Time Homebuyer Programs. Homeownership is not just about having a place to live; it’s about building equity, establishing roots, and securing a future for yourself and your family. These federal initiatives are designed precisely to help you achieve these profound goals.