Navigating 2026 Federal Housing Programs: Updates & Eligibility

Anúncios

As we approach 2026, the landscape of housing in the United States continues to evolve, driven by economic shifts, demographic changes, and ongoing policy discussions. For millions of Americans, the availability and accessibility of safe, affordable housing remain a paramount concern. Recognizing this, the federal government consistently reviews and updates its housing programs to better serve its citizens. Understanding these changes, particularly the nuances of Federal Housing Programs 2026, is crucial for potential homeowners, renters, and housing advocates alike.

Anúncios

This comprehensive guide aims to demystify the anticipated updates, highlight key eligibility changes, and provide actionable insights into navigating the various federal housing initiatives. Whether you are looking to purchase your first home, secure rental assistance, or simply understand the broader implications of federal housing policy, this article will serve as your essential resource for the coming year.

The Importance of Federal Housing Programs

Federal housing programs are the backbone of housing stability for countless individuals and families across the nation. These programs address a wide spectrum of needs, from providing direct financial assistance for rent and utilities to offering pathways to homeownership for low- and moderate-income individuals. The objectives are manifold: to reduce homelessness, promote neighborhood revitalization, ensure fair housing practices, and stimulate economic growth through the housing sector.

Over the years, these programs have adapted to changing economic conditions and societal demands. The updates expected for 2026 are no exception, reflecting a concerted effort to enhance efficiency, broaden reach, and address emerging challenges within the housing market. Staying informed about these developments is not just about compliance; it’s about empowerment—empowering individuals to access the resources they need and empowering communities to build more resilient and equitable housing ecosystems.

Anúncios

Key Agencies and Their Roles in Federal Housing Programs 2026

Several key federal agencies play pivotal roles in the administration and oversight of housing programs. Understanding their functions is essential to grasp the full scope of Federal Housing Programs 2026. The primary players include:

- U.S. Department of Housing and Urban Development (HUD): HUD is the principal agency for housing and community development. It oversees programs related to affordable rental housing, homeownership, fair housing, and homelessness prevention. Its initiatives often form the core of federal housing efforts.

- Federal Housing Administration (FHA): A part of HUD, the FHA insures mortgages made by approved lenders. This insurance protects lenders against losses, making homeownership more accessible, especially for first-time buyers and those with lower credit scores.

- U.S. Department of Veterans Affairs (VA): The VA offers home loan guarantees to eligible service members, veterans, and surviving spouses. These loans often come with significant benefits, such as no down payment requirements and competitive interest rates.

- U.S. Department of Agriculture (USDA): The USDA provides homeownership opportunities in rural areas through various loan and grant programs. These programs are designed to support rural development and ensure access to safe and sanitary housing in less populated regions.

- Treasury Department: While not directly administering housing programs on a day-to-day basis, the Treasury Department plays a crucial role through initiatives like the Low-Income Housing Tax Credit (LIHTC), which incentivizes the creation of affordable rental housing.

Each of these agencies contributes to the multifaceted approach of the Federal Housing Programs 2026, working in concert to address diverse housing needs across the spectrum of American society.

Anticipated Updates and Changes in 2026

While specific legislative details are still being finalized, general trends and policy directions provide a strong indication of what to expect from Federal Housing Programs 2026. These changes are often a response to current economic conditions, housing market trends, and feedback from communities and housing advocates.

Focus on Affordability and Accessibility

One of the overarching themes for 2026 is an increased emphasis on affordability and accessibility. This is likely to manifest in several ways:

- Expanded Rental Assistance: Expect potential adjustments to programs like Section 8 (Housing Choice Vouchers) to address the growing demand for affordable rental units. This could include increased funding, revised income limits, or streamlined application processes.

- First-Time Homebuyer Initiatives: New or enhanced programs aimed at helping first-time homebuyers overcome barriers such as down payment assistance and closing costs are anticipated. These might include expanded eligibility criteria or more flexible loan terms within FHA or conventional loan frameworks.

- Support for Vulnerable Populations: Continued and possibly increased support for special needs populations, including the elderly, disabled, and homeless veterans, through targeted housing programs and supportive services.

Technological Integration and Streamlining

The federal government is increasingly leveraging technology to improve the efficiency and reach of its programs. For Federal Housing Programs 2026, this could mean:

- Digital Application Portals: Further development and widespread adoption of online platforms for applying for housing assistance and loan programs, making the process more user-friendly and accessible.

- Data-Driven Policy Making: Increased use of data analytics to identify areas of greatest need, evaluate program effectiveness, and inform future policy decisions, leading to more targeted and impactful interventions.

- Virtual Counseling Services: Expansion of virtual housing counseling services to provide guidance on homeownership, rental assistance, and financial literacy, particularly benefiting those in remote areas or with mobility challenges.

Sustainability and Resilience

In an era of increasing climate concerns, federal housing programs are also expected to integrate sustainability and resilience measures:

- Energy Efficiency Incentives: Programs may offer incentives for making homes more energy-efficient, reducing utility costs for residents and contributing to environmental sustainability.

- Disaster Preparedness: Enhanced focus on building and rebuilding homes in disaster-prone areas with resilient materials and construction methods, as well as providing assistance for those displaced by natural disasters.

Eligibility Changes: What You Need to Know for 2026

Eligibility criteria are fundamental to accessing federal housing programs. While the core requirements often remain stable, minor adjustments can have significant impacts. For Federal Housing Programs 2026, it’s prudent to be aware of potential changes in income limits, credit requirements, and program-specific conditions.

Income Limits

Income limits are typically set as a percentage of the Area Median Income (AMI) and vary by location and household size. These limits are reviewed annually and are subject to change. For 2026, it’s possible that:

- Adjustments based on inflation and local economic conditions: Income limits may be increased in areas experiencing rapid economic growth or high cost of living, allowing more individuals to qualify. Conversely, they might be adjusted downwards in areas with declining economic conditions, though this is less common for housing assistance programs.

- Categorization of income: There might be clearer guidelines or slight modifications on what constitutes ‘income’ for eligibility purposes, especially concerning non-traditional income sources or benefits.

It is always recommended to check the specific HUD or agency website for the most up-to-date income limits for your particular region when applying for any Federal Housing Programs 2026.

Credit Requirements

For homeownership programs, credit scores play a significant role. While FHA loans are known for their more lenient credit requirements compared to conventional loans, there could be subtle shifts:

- FHA Minimum Credit Scores: While often staying around 580 for a 3.5% down payment, there might be slight upward or downward adjustments based on market risk assessments. Applicants with lower scores (e.g., 500-579) may still qualify but typically require a larger down payment.

- Credit Counseling Emphasis: An increased emphasis on mandatory credit counseling for applicants with borderline credit scores to improve financial literacy and reduce default risks.

- Alternative Credit Data: A potential exploration or pilot programs to consider alternative credit data (e.g., rent payment history, utility payments) to assess creditworthiness, particularly for individuals with thin credit files.

Program-Specific Conditions

Each federal housing program has unique conditions that borrowers or applicants must meet. These can include:

- Occupancy Requirements: For FHA, VA, and USDA loans, the property typically must be the borrower’s primary residence. Any changes to these requirements would be significant.

- Property Standards: Properties financed through federal programs must meet certain health and safety standards. There might be updated guidelines for energy efficiency or lead-based paint remediation.

- Veteran Status Verification: For VA loans, the process for verifying veteran status and eligibility might be streamlined or updated.

Staying abreast of these specific conditions for each program under Federal Housing Programs 2026 is vital for a successful application.

Navigating Homeownership Programs in 2026

For many, homeownership is a cornerstone of financial stability and personal well-being. Federal Housing Programs 2026 offer several avenues to achieve this goal, especially for those who might face challenges in the conventional market.

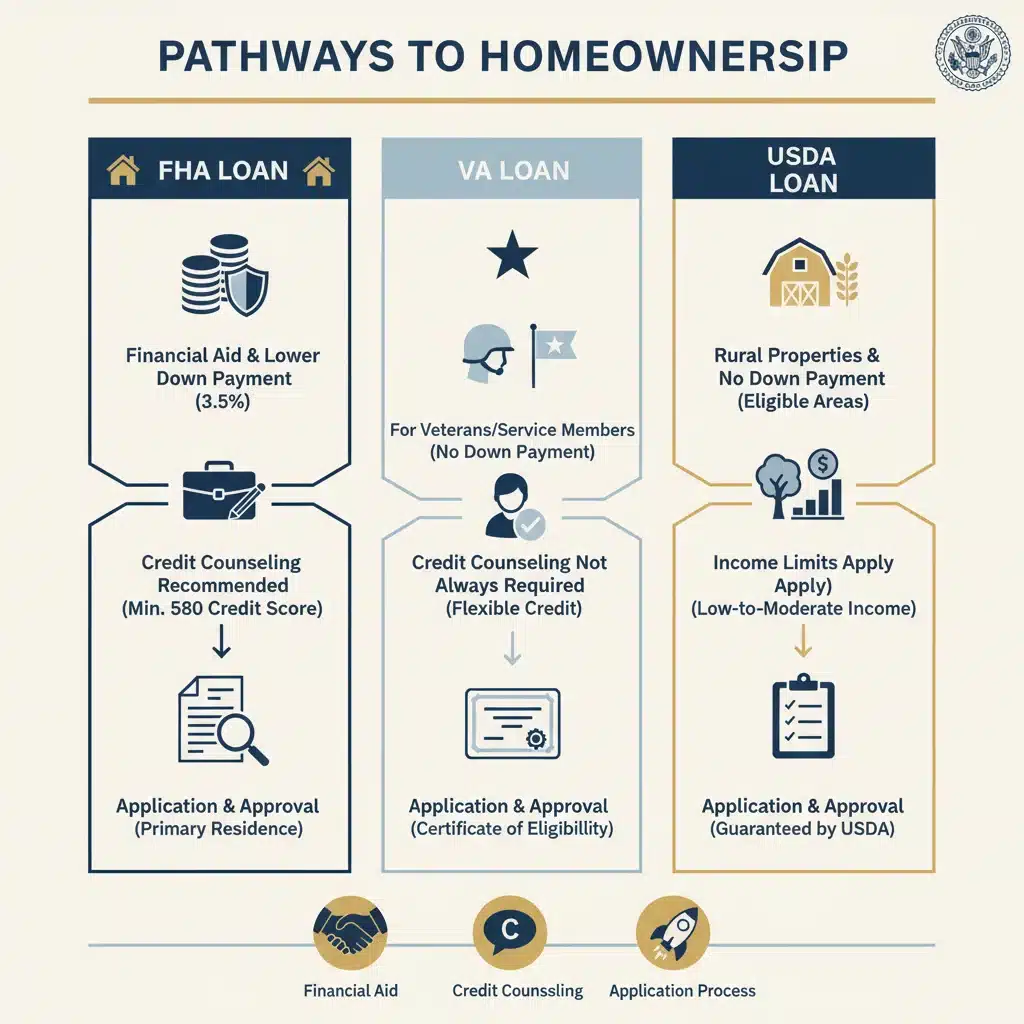

FHA Loans: A Pathway for Many

FHA loans continue to be a popular choice for first-time homebuyers and those with less-than-perfect credit. The benefits include lower down payment requirements (as low as 3.5%) and more flexible credit score guidelines. For 2026, potential considerations include:

- Mortgage Insurance Premiums (MIP): FHA loans require both an upfront and annual MIP. While these are subject to regular review, any changes could impact the overall cost of the loan.

- Loan Limits: FHA loan limits are adjusted annually based on housing costs. Expect updated limits for 2026, which will determine the maximum loan amount you can receive in your area.

- Streamlined Refinance Options: Continued availability and potentially enhanced options for FHA streamlined refinances, allowing current FHA borrowers to reduce their interest rates and monthly payments with minimal paperwork.

VA Loans: Honoring Service Members

VA loans are an unparalleled benefit for eligible service members, veterans, and surviving spouses. Key advantages include no down payment requirement, no private mortgage insurance (PMI), and competitive interest rates. Updates for Federal Housing Programs 2026 related to VA loans might involve:

- Funding Fee Adjustments: The VA funding fee, which is a one-time payment required on most VA loans, can change. Exemptions for certain disabled veterans are likely to remain.

- Expanded Eligibility: While core eligibility remains tied to service, there could be minor expansions or clarifications for specific service periods or circumstances.

- Native American Direct Loan (NADL) Program: Continued focus on the NADL program, which helps Native American veterans purchase, construct, or improve homes on Native American trust land.

USDA Loans: Rural Homeownership Opportunities

The USDA Rural Development loan program is crucial for promoting homeownership in designated rural areas. These loans offer 100% financing, making them highly attractive. For 2026, watch for:

- Updated Eligibility Maps: The USDA periodically updates its maps of eligible rural areas. It’s essential to check if your desired location still qualifies for a USDA loan.

- Income Limit Revisions: Income limits for USDA loans are specific to rural areas and are subject to annual review.

- Emphasis on Energy-Efficient Homes: Potential incentives or preferences for homes that meet certain energy efficiency standards within the USDA loan program.

Rental Assistance Programs in 2026

Beyond homeownership, Federal Housing Programs 2026 also heavily focus on ensuring affordable rental options for those who need them most. These programs are vital in preventing homelessness and maintaining housing stability.

Housing Choice Vouchers (Section 8)

The Housing Choice Voucher program, commonly known as Section 8, is HUD’s largest program for assisting very low-income families, the elderly, and the disabled to afford decent, safe, and sanitary housing in the private market. Anticipated updates for 2026 could include:

- Increased Funding: A potential push for increased congressional appropriations to address the long waiting lists often associated with this program.

- Fair Market Rent (FMR) Adjustments: FMRs, which determine the maximum rent a voucher can cover, are updated annually. Expect these to be revised for 2026, reflecting local rental market conditions.

- Portability Enhancements: Efforts to make it easier for voucher holders to move across jurisdictions, increasing housing choices and reducing barriers to relocation for employment or family needs.

Public Housing

Public housing, managed by local Public Housing Agencies (PHAs), provides affordable housing for low-income families, the elderly, and persons with disabilities. While new public housing developments are less common, the focus remains on maintaining and modernizing existing stock. For 2026, expect:

- Capital Fund Program (CFP) Allocations: Continued funding through the CFP to PHAs for major repairs, renovations, and energy efficiency upgrades.

- Rental Assistance Demonstration (RAD): Ongoing conversions under the RAD program, which allows PHAs to leverage private financing to address capital needs while preserving long-term affordability.

Other Rental Assistance Initiatives

Several other programs contribute to rental affordability:

- Project-Based Rental Assistance (PBRA): Continued support for PBRA, where subsidies are tied to specific housing units, making them affordable for low-income tenants.

- Emergency Rental Assistance (ERA): While largely a COVID-19 response, there might be discussions about more permanent or flexible emergency rental assistance mechanisms within Federal Housing Programs 2026 to address unforeseen financial hardships.

Fair Housing and Anti-Discrimination Efforts

A cornerstone of federal housing policy is the commitment to fair housing and the prevention of discrimination. The Fair Housing Act prohibits discrimination in housing based on race, color, national origin, religion, sex (including gender identity and sexual orientation), familial status, and disability. For 2026, expect:

- Enhanced Enforcement: Continued vigorous enforcement by HUD and the Department of Justice against discriminatory practices in housing.

- Affirmatively Furthering Fair Housing (AFFH): Potential re-emphasis or revised guidance on the AFFH rule, which requires federal agencies and grantees to take proactive steps to overcome patterns of segregation and foster inclusive communities.

- Education and Outreach: Increased efforts to educate both housing providers and consumers about their rights and responsibilities under the Fair Housing Act.

How to Prepare and Apply for Federal Housing Programs in 2026

Understanding the programs is the first step; knowing how to effectively apply is the next. Given the potential updates to Federal Housing Programs 2026, proactive preparation is key.

For Homeownership Programs:

- Improve Your Credit Score: Start early by checking your credit report for errors and working to improve your score. Pay bills on time, reduce debt, and avoid opening new credit lines.

- Save for a Down Payment and Closing Costs: Even with low down payment options, having some savings is beneficial. Research potential down payment assistance programs available at the state or local level, which can often be combined with federal loans.

- Gather Financial Documents: Collect income statements, tax returns, bank statements, and other financial records. Having these organized will expedite the application process.

- Seek Pre-Approval: Get pre-approved for a loan to understand your borrowing capacity and show sellers you are a serious buyer.

- Work with a Knowledgeable Lender: Choose a lender experienced in FHA, VA, or USDA loans who can guide you through the specific requirements of Federal Housing Programs 2026.

- Attend Housing Counseling: Especially for first-time buyers, HUD-approved housing counseling agencies offer invaluable advice on the homebuying process, financial management, and avoiding predatory lending.

For Rental Assistance Programs:

- Contact Your Local PHA: Public Housing Agencies (PHAs) administer most rental assistance programs. Visit their website or call them to inquire about application procedures, waiting lists, and specific eligibility requirements for Federal Housing Programs 2026 in your area.

- Prepare Documentation: Be ready to provide proof of income, household composition, identification, and any disability or veteran status documentation.

- Understand Waiting Lists: Many rental assistance programs have long waiting lists. Apply as soon as possible and periodically check on your application status.

- Be Aware of Preferences: Some PHAs give preference to certain populations, such as the elderly, disabled, or homeless. Understand if you qualify for any preferences.

- Report Changes Promptly: If your income or household composition changes while on a waiting list or receiving assistance, report it immediately to your PHA.

The Broader Impact of Federal Housing Programs 2026

The reach of Federal Housing Programs 2026 extends far beyond individual beneficiaries. These programs have significant macroeconomic and social impacts:

- Economic Stimulus: Housing construction and sales generate jobs, stimulate local economies, and contribute to GDP. Federal programs can stabilize and boost these sectors.

- Community Development: By providing resources for affordable housing and neighborhood revitalization, programs contribute to stronger, more vibrant communities.

- Reduced Inequality: Ensuring access to safe and affordable housing helps reduce wealth and opportunity gaps, fostering greater social equity.

- Improved Health and Education Outcomes: Stable housing is linked to better health outcomes, improved educational attainment for children, and increased overall well-being.

As the federal government continues to invest in these critical areas, the positive ripple effects are felt across the entire nation, contributing to a more stable and prosperous society.

Staying Informed Beyond 2026

The housing landscape is dynamic, and federal programs are continuously evaluated and adjusted. To stay informed beyond the immediate updates for Federal Housing Programs 2026, consider these strategies:

- Subscribe to Government Updates: Sign up for newsletters and alerts from HUD, FHA, VA, and USDA websites.

- Follow Reputable Housing News Sources: Stay updated through national and local news outlets that cover housing policy.

- Consult Housing Counseling Agencies: These agencies are often the first to receive updates on program changes and can provide personalized advice.

- Engage with Local Housing Authorities: Your local PHA is a direct source of information for programs specific to your community.

Conclusion

The Federal Housing Programs 2026 represent a critical component of the nation’s efforts to ensure that all Americans have access to safe, decent, and affordable housing. From facilitating homeownership through FHA, VA, and USDA loans to providing essential rental assistance via Section 8 and public housing, these initiatives are designed to address a diverse array of housing needs.

Anticipated updates, focusing on affordability, technological integration, and sustainability, underscore the government’s commitment to adapting to current challenges and fostering more equitable housing opportunities. By understanding the roles of key agencies, familiarizing yourself with potential eligibility changes, and preparing diligently for the application process, you can effectively navigate these programs and take significant steps toward achieving your housing goals.

Whether you are a prospective homeowner, a family seeking rental stability, or an advocate for housing justice, staying informed about the evolving landscape of federal housing policy is not just beneficial—it’s essential for building a more secure and prosperous future for all.